top of page

charles

FRAUD

Expose Truth.Fight Injustice.Demand Action.

DISSY AWARDS ARCHIVE

DISCIPLINARY ACTION OF THE MONTH

NOVEMBER 2025

And the Dissy Goes To...

TD AMERITRADE

c/o Charles Schwab

.jpg)

View the official FINRA Letter of Acknowledgement, Waiver, and Consent (A.W.C.) pertaining to this disciplinary action:

Schwab/TD Ameritrade A.W.C. NO. 2021070230801

FINRA Disciplinary Actions - November 2025:

Disciplinary actions November 2025

View the official "FINRA Letter of Acceptance, Waiver, and Consent" pertaining to this disciplinary action:

FINRA A.W.C. O. 2021070230801

View FINRA's Monthly Disciplinary Actions for November 2025 (or access from FINRA's site here)

FINRA disciplinary actions - November 2025

.jpg)

NOVEMBER 2025 DISSY AWARD TD AMERITRADE AND SCHWAB

Charles Fraud hereby recognizes TD Ameritrade for their continued dedication to continuous avoidance of consequences for two full decades worth of persistent rule-breaking and recordkeeping "errors" that corroded the authenticity of the audit trail, for untold "millions" of transactions, with their true significance and impacts likely to remain concealed forever.

Of course, as Schwab and TD Ameritrade have now merged (after colluding while "competitors" in 2018 and perhaps earlier), the disciplinary action and the Dissy award are formally issued to Charles Schwab and Co., Inc.

One of the primary shortcomings of FINRA's disciplinary "actions" is that they actually represent an agreement that no future action will be taken based on the "factual findings." This "action" is exemplary because the duration of TD Ameritrade's violative behavior covered here spans "from at least January 2007 to February 2022" and an unspecified total number of transactions in addition to the millions mentioned.

From page 1 of the A.W.C.,

"This AWC is submitted on the condition that, if accepted, FINRA will not bring any future actions against Respondents alleging violations based on te same factual findings described in this AWC"

2. IMPROPER REPORTING TO FNTRG and ORF

Millions of transactions were either not reported or delayed reporting of other transactions were to the FNTRG and ORF. As such, this hinders FINRA's ability to detect fraud and other wrongdoing "from at least January 2007 to February 2022":

From page 3 of the A.W.C.,

As set forth in the A.W.C. (page 3):

The FNTRF and ORF provide member firms with a mechanism by which to report transactions effected other than on an exchange. The data that members report has a direct impact on the accuracy of public information FINRA disseminates. Additionally, the inaccurate reporting of required trade information may negatively impact FINRA’s surveillance patterns. FINRA relies on the accuracy of trade reporting to reconstruct and review the activities of market participants to safeguard the integrity of the securities markets and protect investors.

And what do those "factual findings" entail?

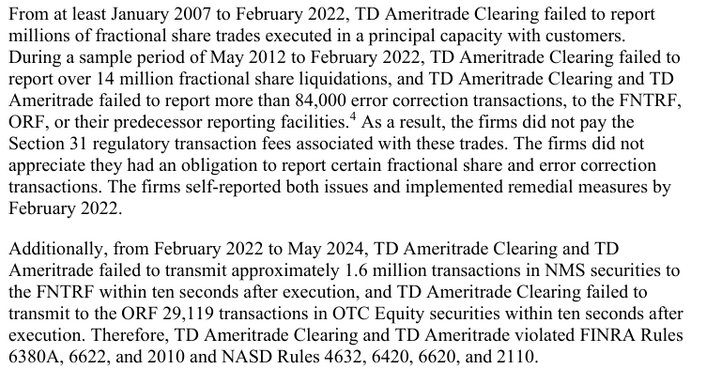

1. FAILURE TO REPORT FRACTIONAL SHARE TRADES

"From at least January 2007 to February 2022", TD Ameritrade failed to report millions of fractional share trades executed in a principal capacity with customers. The exact number is not stated, but 14 million such transactions failed to be reported during a "sample period" from May 2012 to Feb 2022.

Excerpt from A.W.C. NO. 2021070230801 (page 3):

3. FAILURE TO REPORT EQUITY AND INDEX POSITIONS & POSITION CHANGES

From July 2020 to March 2022, TD Ameritrade Clearing failed to report equity and index options position changes to the LOPR in 59,238 instances when a position was added, modified, or deleted on the expiration date of the option.

3b. TD Ameritrade Clearing failed to report equity and index options positions to the LOPR in 12,118 instances when its system caused certain accounts acting in concert to be randomly missed.

From page 4 of the A.W.C.,

4. No written supervisory procedures for reporting error correction transactions

Buried on the fifth page of the A.W.C., it was found that TD Ameritrade was NEVER in compliance regarding "reporting of error correction transactions" before they merged with Schwab.

"From 2007-2024... neither TD Ameritrade Clearing nor TD Ameritrade had written supervisory procedures concerning the reporting of error correction transactions prior to terminating their FINRA membership in 2024."

From pages 4-5 of the A.W.C.,

As set forth in the A.W.C. (page 3):

"FINRA requires member firms to report large options positions to the Large Options Positions Reporting (LOPR) system. FINRA uses LOPR information to identify holders of large options positions and to surveil for potentially manipulative behavior, including attempts to corner the market in the underlying equity, leverage an option position to affect the price, or move the underlying equity to change the value of a large option position. The accuracy of LOPR reporting is essential to FINRA’s surveillance. It is particularly important with respect to the over-the-counter (OTC) options market because there is no independent source of data for regulators to review OTC options."

Many questions remain unanswered, such as:

Underlying positions and patterns

Which specific underlying stocks or index funds were misreported, and did the misreporting exhibit any consistent patterns or biases (e.g., by product type, issuer, or strategy)?

Unreported transactions vs. account errors

Did any unreported transactions coincide in time with erroneous accounting entries and/or omitted positions in clients’ accounts? If so, how many such instances were identified and over what period?

Lack of procedures for error corrections

If there was no written procedure for reporting error-correction transactions (see #4 above), does that mean there was no established, standardized method for handling and documenting actions taken when “errors” required “correction”?

Duration and extent of erroneous reporting

What does it mean that erroneous reporting occurred "from at least January 2007 to February 2022" mean? (#1) How much longer before 2007 could this problem have persisted. And, could this issue be related to the reporting requirements that TD Ameritrade NEVER complied with? (#4)

Well, since this is now a settled matter, there will be no further inquiries by the authorities, so it's unlikely that we'll ever have any answers.

Bravo! This excellence in avoidance is a well deserving

of the November DISSY AWARD!

APRIL 2025

And the Dissy Award Goes To... MarketAxess Corporation

DISCIPLINARY ACTION OF THE MONTH

Charles Fraud hereby recognizes MarketAxess Corporation for their "pattern and practice" of misreporting trade execution times to the Real-time Transaction Reporting System (RTRS) due to the firm's "incorrect interpretation of the time of trade" and, additionally, for similar issues due to "technological errors" that caused inaccurate and untimely transaction reporting to the Trade Reporting and Compliance Engine (TRACE). The majority of the misreported transactions were inaccurate by only one second - which may not seem particularly severe, but there are several issues that make this "Disciplinary Action" stand out, and a deeper dive confirms that it is genuinely worthy of the DISSY award.

"MarketAxess reported 57,340 [municipal securities] transactions to the RTRS with an inaccurate time of trade due to the firm’s incorrect interpretation of time of trade. For a majority of these transactions, the execution time was inaccurate by one second." MarketAxess A.W.C. FINRA NO. 2020065254901, p.3.

Also, 51,252 corporate bond transactions and 2,446 U.S. Treasury transactions were reported to TRACE with inaccurate transaction times. "For about half of these transactions, the time of execution was inaccurate by one second... These inaccurate and late reports occurred due to a technological error..." MarketAxess A.W.C., p.3.

While a one second deviation may seem insignificant, that is more than enough time to exploit and conceal manipulative and abusive trading. Generally, in electronic trading (and especially in the context of high-frequency algorithmic trading), where many strategies rely on quick responses to real‑time data, even a one‑second deviation can be exploited into an unfair advantage, including Shadow Front Running of Customer Orders and/or concealing Matched-Book or Wash Trades - more on that below. To be fair, nothing of this sort is reported in this A.W.C., but there is nothing to suggest that any serious inquiry was made by FINRA in this regard, either.

The deciding factor for awarding this Dissy was that, even after new measures were implemented "to ensure that accurate execution times were reported to TRACE and RTRS", THE PROBLEMS CONTINUED, AND THERE IS NO MENTION OF THE ISSUE EVER BEING RESOLVED. Astoundingly, the inaccurate times continued to be attributed to the firm's "incorrect interpretation of the meaning of time of trade." p.4

From FINRA MarketAxess A.W.C. NO. 2020065254901 - page 4 (literally as a footnote):

"After January 2022 when the firm began performing automated surveillance and manual reviews of surveillance alerts, the firm continued to report certain municipal bond transactions to RTRS with inaccurate times of trade due to its incorrect interpretation of the meaning of time of trade."

But since this is now a settled matter, and so long as MarketAxess "accepts and consents to the findings without admitting or denying them" and pays the $180,000 fine, the firm may now exempt from further action regarding this matter... even for problems that continued after remedial measures were taken and which may still be unresolved because, of course, this A.W.C. contains the standard boilerplate verbiage:

"FINRA will not bring any future actions against Respondent alleging violations based on the same factual findings described in this AWC." p.1

So, perhaps MarketAxess continues to operate with an "incorrect interpretation of the meaning of time of trade" and...

NO FURTHER ACTION CAN BE TAKEN REGARDING THIS MATTER.

Congratulations! That is an impressive feat well-deserving of a DISSY!

The Dissy

No other details were provided that could answer the following questions:

What caused the firm to have an "incorrect interpretation of the time of trade"? What does this even mean? And why is this such a difficult matter to resolve?

What were the nature of the "technological errors" that caused the untimely reporting? And why were only some transactions reported inaccurately?

The A.W.C. states that half or more of the erroneous timestamps were 1s late. So, there are many inaccurately reported transactions erroneous by something other than 1 second. Was there more than one error? Were there additional types of "incorrect interpretation of time of trade"?

Did anyone investigate whether Front Running, Matched-Book or Washed Trades, or other exploitative or manipulative activities were facilitated by or otherwise coincided with these errors? DID FINRA EVEN INQUIRE?

Lastly, a couple examples explaining how reporting transactions late by one second could be exploited for manipulative purposes:

SHADOW FRONT RUNNING

Suppose a customer order arrives at time zero seconds 0.00s. The firm could front-run the transaction and purchase at time 0.5s. If the execution time of the customer order is delayed by one second, reported as executed at time 1.00s, then surveillance would show the firm's own trade occurring before the customer and thus would not be flagged for front-running.

HIDING MATCHED-BOOK OR WASHED TRADES

Suppose the firm executes both sides of a risk‑free flip (buy → sell) (or is acting in concert with another market participant). By forward-shifting the timestamp of the final transaction by +1s (or more), this can camouflage and prevent detection of exploitative trading to manipulate asset prices.

DISCIPLINARY ACTION OF THE MONTH

MARCH 2025

And the Dissy Award Goes To... UBS Financial Services!

Charles Fraud hereby recognizes UBS Financial Services, Inc. for submitting 17,000 Blue Sheets that misreported, or failed to report information about 4.4 million transactions due to "coding errors." UBS was fined $1.1 million, just $.25 per misreported blue sheet. UBS began revising the coding issues in November 2017, and by September 2018 "all of the logic impacting the transaction fields was remediated."

No other details were provided regarding the following :

The Dissy

Excerpt from page 2 of FINRA AWC NO. 2019061777501

-

What actually caused the "coding errors"?

-

Why did it so long to notice or to fix the problems? Also, why don't FINRA's Monthly Disciplinary Actions report how long it took for UBS to fix the "logic."

-

Were all issues remediated, or just the "logic impacting the transaction fields"?

-

Did the issues impact only the Blue Sheet reporting data, or did it also cause problems with (or perhaps originated from) their transaction and accounting systems?

Well, since this is now a settled matter, there will be no further inquiries by the authorities, so it's unlikely that we'll have those answers.

Bravo! This fecklessness is well deserving of the inaugural DISSY AWARD!

Electronic Blue Sheets (EBS) | FINRA.org:

Electronic Blue Sheet (EBS) data files, which contain both trading and account holder information, provide regulatory agencies with the ability to analyze a firm’s trading activity. Firms are expected to provide complete, accurate and timely Blue Sheet data in response to regulatory requests. Incomplete, inaccurate and untimely Blue Sheet data compromises regulators’ ability to identify individuals engaging in insider trading schemes and other fraudulent activity.

bottom of page